Taking negative revisions into account, jobs actually rose by 77,000, while unemployment rises as job seekers fail to find jobs. Bloomberg labeled this “Rites of Gold.”

Please note the Bureau of Labor Statistics Monthly payroll report for July

Initial Thoughts

- A gain of 187,000 looks good, but negative revisions of 110,000 remove any semblance of OK.

- Employment rose by 222,000, but unemployment rose by 514,000. More than half a million people wanted work but could not find it.

- The non-institutional civilian population is 267,213,000 inhabitants. Employment is 161,484,000. This means that there are nearly 106 million people aged 16 and over who are not working at all.

- Because of the annual benchmark revisions, the way the BLS reports revisions, and the relatively small sample sizes of the monthly employment reports, we cannot suggest with much confidence that these reports represent an accurate picture of the jobs or employment.

Non-farm payrolls and employment levels

About these strong jobs reports: Full-time employment has fallen by 150,000 since January 2023.

Payrolls vs employment gains since May 2022

- Non-agricultural payrolls: 4,377,000

- Employment level: +3,185,000

- Full-time employment: +1,446,000

- Only 45.4 percent of employment gains over the past 15 months were full-time employment.

Of the 894,000 increase in employment in January, 810,000 were due to annual benchmark revisions. And the BLS doesn’t say which months were reviewed, just poof, there you go. Again, we cannot, with great confidence, suggest that these reports portray an accurate picture of jobs or employment..

Job report details

- Non-agricultural payroll: +187,000 to 156,419,000 – Survey in the establishment

- Non-institutional civilian population: +211,000 to 267,213,000

- Civilian labor force: +736,000 to 167,839,000 – Household survey

- Participation rate: +0.2 to 62.8% – Household survey

- Employment: +222,000 to 161,484,000– Household survey

- Unemployment: +514,000 to 6,355,000- Household survey

- Reference unemployment rate: +0.3% to 3.8% – Household survey

- Not in the active population: 525,000 to 99,374,000 – Household survey

- Under-6 unemployment: +0.4 to 7.1% – Household survey

Change of non-agricultural payrolls

Monthly reviews

- August 2023: The change in total nonfarm payroll employment for June was revised down by 80,000 from +185,000 to +105,000and the July change was revised down by 30,000, from +187,000 to +157,000. With these revisions, employment in June and July combined is 110,000 less than previously reported..

- July 2023: The change in total nonfarm payroll employment for May was revised down by 25,000 from +306,000 to +281,000, and the The June change was revised down by 24,000 from +209,000 to +185,000. With these revisions, employment in May and June combined is 49,000 fewer than previously reported.

Last month, the BLS revised the net gain in June from 209,000 to 185,000. This month, the BLS revised June from 185,000 to 105,000.

Expect more negative reviews.

Part-time jobs

- Involuntary part-time work: +197,000 to 4,221,000

- Voluntary part-time work: +4,000 to 21,975,000

- Total full time job: -85,000 to 134,189,000

- Total part-time work: +32,000 to 27,185,000

The numbers above never add up correctly because of the way the BLS makes seasonal adjustments. I list them as reported.

Full-time employment fell by 585,000 in July and another 85,000 this month.

Hours and Wages

This data is reviewed frequently.

- Average weekly hours of all private employees increased by 0.1 hours to 34.4 hours.

- The average weekly hours of all employees providing private services was flat at 33.3 hours.

- Manufacturers’ average weekly hours were flat at 40.1 hours.

An overall decrease or increase of one-tenth of an hour doesn’t sound like much, but with 160 million jobs, it’s more significant than meets the eye.

A year ago, the average total private weekly hours was 34.5 hours.

Earnings per hour

This data is also reviewed frequently. Here are the numbers that were reported this month.

Average hourly earnings of all non-farm workers rose $0.08 to $33.82. A year ago the average wage was $32.43. This represents a gain of 4.3%.

Average hourly earnings of production and non-supervisory workers rose $0.06 to $29.00. A year ago the average wage was $27.75. This represents a gain of 4.5%.

Year-over-year wages are finally catching up with inflation after underperforming for many months. However, wage growth is slowing. The monthly increase in production workers in August was just 0.2 percent.

Unemployment

The unemployment rate hit a 50-year low in January and 3.4 percent in April. This month it is 3.8 percent. It is the highest since February 2022.

Alternative unemployment measures

Table A-15 is where one can be found better approximation of what the unemployment rate actually is.

The official unemployment rate is 3.8%.

U-6 is much higher at 7.1%. Both figures would be much higher if it weren’t for the millions who have left the workforce in recent years.

Some of those who left the workforce retired because they wanted to retire. Some left due to fears of Covid and never returned. Still others took advantage of a strong stock market and took early retirement.

The rest is disability fraud, forced retirement (need for Social Security income) and discouraged workers.

Birth death model

As of January 2014, I left the Birth/death model graphics in this report.

The birth-death model concerns the birth and death of corporations, not individuals, except by implication.

For those who keep track of the numbers, I keep this caution: Do not subtract the reported birth-death number from the reported holder number. This approach is not statistically valid.

The model is wrong at economic turning points and is also heavily revised and therefore essentially useless.

Household survey vs. payroll survey

- The payroll survey (sometimes called the establishment survey) is the primary job count. It is based on employer reports.

- The household survey is a telephone survey conducted by the BLS. It measures employment, unemployment and other factors.

If you work an hour, you are busy. If you don’t have a job and you’re not looking for one, you’re not considered unemployed, you’re leaving the labor force.

Searching for jobs on Jooble or Monster or in job ads does not count as “job searching”. You need a real interview or send a resume.

These distortions artificially lower the unemployment rate, artificially increase full-time employment, and artificially increase the payroll jobs report each month.

Golden waterfalls!?

Check back on these porridges in a little while.

Expect a long but shallow recession with a minimal increase in unemployment

Given the hiring pressures and boomer retirements, Ewait for Long but shallow recession with minimal increase in unemployment

Unlike many others, I expect that the unemployment rate will not rise much in this recession compared to the average impact of the recession. Employment due to the retirement of baby boomers is another matter.

Job offers and resignations are in sharp decline. The Fed will be happy.

Please note Job offers and resignations are in sharp decline. The Fed will be happy.

I The labor leverage ratio, a measure of wage bargaining power, is in decline.

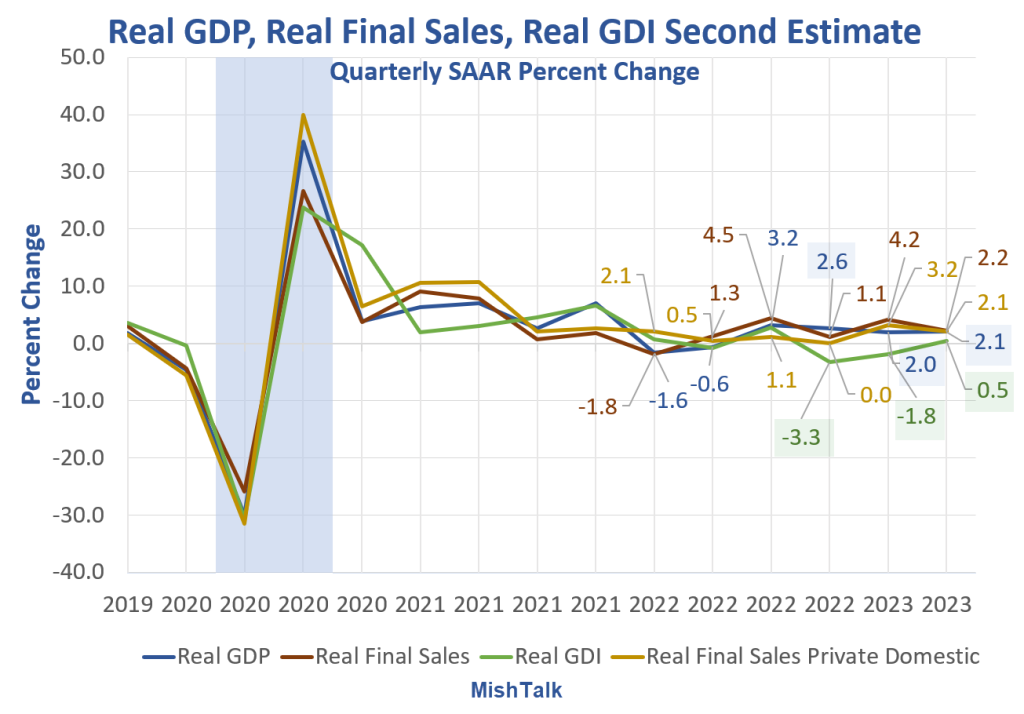

Negative revision of Q2 GDP, large discrepancy with GDI continues

Large discrepancy between GDP and GDI

On August 30, I noticed negative Review tor GDP in the 2nd quarter, the large discrepancy with the GDI continues

Large discrepancy between GDP and GDI

GDP and GDI are two measures of the same thing, one from a product perspective, the other from an income perspective. Over time they merge.

The last three quarters of GDP from the fourth quarter of 2022 are 2.6 percent, 2.0 percent and 2.1 percent. The last three quarters of GDI from 4Q 2022 are -3.3 percent, -1.8 percent and 0.5 percent.

GDI is still consistent with a recession starting in Q4 2022. GDP is not. The NBER, the official arbiter of recessions, averages the two measures. The result is inconclusive for Q4 and Q1 combined.

Don’t be surprised if the NBER declares that we’ve had a recession and it’s over. It’s happened before.

Employment data is very consistent with GDP, not GDP. Also, jobs in the economic swings are one of the most reviewed measures.

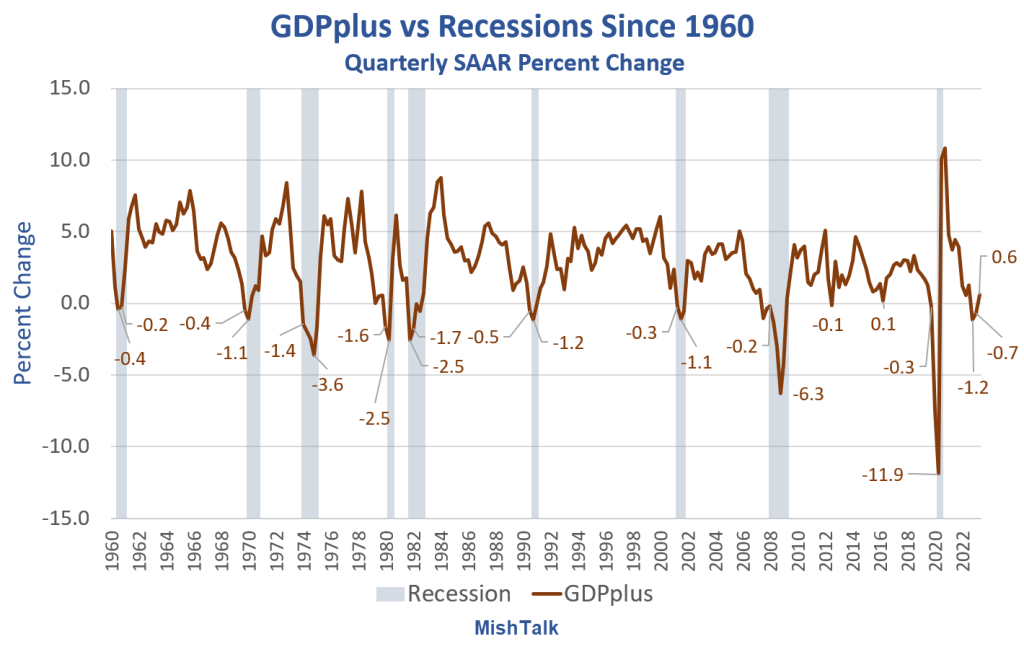

Philadelphia Fed’s GDPplus measure looks like recession started in Q4 2022

PIBplus is a measure of the quarter-on-quarter growth rate of real output in continuously compounded annualized percentage points.

It is a combination, but not an average, of gross domestic product (GDP) and gross domestic income (GIR). It is much softer than GDP or GDI, as the chart above shows.

For Q4 2022 and Q1 2023, the PIBplus figures are -1.2% and -0.7%, respectively.

For discussion, see philadelphia Fed The PIBplus measure looks like a recession started in Q4 2022

100 percent of the time, with no false signals, no errors, and no lead times longer than two quarters, every time GDPplus had two consecutive quarters of negative growth, the economy was in recession.

On closer inspection, except for a reading of -0.1 percent, every time GDPplus was negative for even a quarter, a recession soon followed.

Ignoring a barely negative impression, GDPplus does not give false positives. And the delay is short compared to the performance curve analysis.

The caveat is GDI and therefore GDPplus are revised frequently. But the latest revision was from -0.4% for the first quarter of 2023 to -0.7%.

This analysis clearly points to a recession starting in Q4 2022. Maybe we had a recession and nobody noticed. Don’t worry, there will be another one.